If you’re looking for a budget to use as we head into 2023 to get your financial life back in order, then here is the best personal budget template in excel. It’s not even subjective, it’s 100% literally the best budget financial template you can use.

Now, I may be biased because I created this budget…and all jokes aside, it is entirely subjective. What works for me may not work for you. But what I tried to create with this financial template is something that is completely designed for people who live paycheck to paycheck and want to set goals to move beyond that.

And last I checked nearly 4 out of 5 Americans are more less living this way, and about 40% of the population are a paycheck away from poverty.

This means we need a budget template that is fit for that.

Now the template I’m mentioning here not only tracks your budget but your net worth as well. And this is a complete game changer. Personally, once I started tracking my net worth I started making much better financial decisions.

If you can pull this off you’ll be ahead of 95% of the population (I completely made that number up).

Now in addition to that, the template is “hands on” but not too much so. Basically you’ll sit down to do your budget every time you get paid, pay your bills and you’ll be set with not only a budget for the next couple of weeks, but one that projects months into the future as well.

Personal Budget Template Download

With that being said you can get this personal budget template on Etsy.

The full version of this excel template will track your budget, net worth, discretionary income, credit utilization, as well as debt to income ratio.

Now to be completely clear, this isn’t some overly complicated excel template that has tons of formulas that only someone who can code could possibly figure out. If you’re experienced with excel could likely copy this yourself and make your own version of it if you want to avoid paying a small charge for the full version.

But if you’ve read this site at all you know that time is money, and I assure you you’re coming out ahead on the time vs. money ratio regardless of your income if you want to purchase it.

Simplicity is Ideal for a Financial Template

Now I tried several different apps before just ending on using an excel budget template instead. Mint is probably the most popular application you can use to track your budget. Personally, this, and others like this, are just too much for me personally.

They basically pull all of your data from your banking account. This to me is red flag number 1. First of all, I don’t want to give them access to my bank account. That’s just me though.

The other issue I came across from using applications is that they just have way too much on them that isn’t necessary and really don’t matter in your life. Yeah they come up with a cool looking chart, but there is nothing there that gives a full viewpoint of my budget without overcomplicating things like I was able to create by using my own excel budget template.

And finally, when an application is automating all of your spending/info etc. it really doesn’t give you much of a hands-on approach. And while you don’t want to manually do everything, you do want to understand what (and when) your bills are.

Using excel as your financial budget template gives you access to see your full budget in front of you, even months in advance.

Why You Need to Track Your Net Worth

As I mentioned tracking your net worth alongside your budget is going to put you ahead of most of the population in terms of setting yourself up for financial success.

The full version allows you to track all of your debts and assets and then tracks your net worth. It also gives a couple different alternatives on calculating your net worth to give you different viewpoints and potential goals to set for yourself.

Essentially, knowing exactly what is coming out of your budget each month and then being able to have a full picture of all of your assets vs. debts is really what you need in order to set yourself up to be successful.

With that being said, let’s get into it.

Budget Template Tutorial

To get started you’ll have to add all of your bills, income, etc. to get moving. Once you add everything it’s pretty automated from there.

Now you can utilize any of the tabs on this template you want, but clearly the most important portion is the budget tracking section of it. As you see it comes with 3 different options to use: weekly, bi-weekly, or monthly.

All you need to do is add the first date you get paid and all of the other dates will automate in for the weekly and bi-weekly tabs, the tracker is pre-set for the first payment date as Dec. 30, 2022 as this is a Friday and the last day of the year, so if that wasn’t the last pay date for you you’ll need to change that to your pay date and all future dates will autofill in.

Now if you are using the monthly option, you will have to enter the dates if it doesn’t match the preset dates. The monthly option is preset with pay dates set as the last business day of each month.

Choose which option you want (weekly, bi-weekly, or monthly) and you can delete the other 2 tabs if you don’t need them.

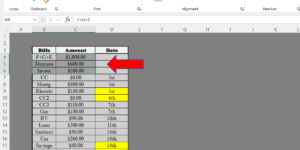

For the tutorial we’ll use biweekly since that’s the most common way people get paid. Now the first thing to do get started is to add all of your bills, and we’ll be doing this under the “bills” tab prior to adding anything into the budget area.

Be sure to add your bills in order by date and highlight anything that is on auto pay yellow (or whichever color you want) over the date. This is necessary to smoothly add everything into your budget.

You can always sort the dates after adding in all of your bills by highlighting just that section and then choosing “sort and filter” and then going down to “custom sort” and then sorting the dates.

Next, you’ll add bills to the “budget tab”.

Certain things you pay like food, gas, and entertainment won’t be a monthly bill. Or with the example we’re using, also daycare and $100 added to investments are included in the example.

Personally I add food, gas, and entertainment (F+G+E) as one complete category and have found this as the easiest approach. Of course you can choose to separate these if you want, however, this adds a lot of manual calculating. Adding this in one category makes sense because all of these are something that you can control. If the number comes up too high then you can always do a separate audit.

Things like this won’t have dates since they will be added to your budget every 2 weeks as opposed to monthly. Start with simply copying all of these and adding them to the budget section.

Highlight the bills to copy by pressing control+C.

After you’ve highlighted the bills you want to copy over, paste them under the budget “biweekly” section using control+V.

Above we added all expenses that don’t have a monthly date, next we’ll add all of our bills with monthly dates to the budget section the same way.

Above we added all expenses that don’t have a monthly date, next we’ll add all of our bills with monthly dates to the budget section the same way.

Next, add in your income. There are several sections here added that you may not need. If that’s the case, you may want to add some extra sources of income 😉

Next, add in your income. There are several sections here added that you may not need. If that’s the case, you may want to add some extra sources of income 😉

Either way, add what you make and rename them if you want. The budget will be set with 2 base pay options, 2 bonus options, 1 side hustle option, and 1 additional column. You can delete added rows if you don’t want all of the options available.

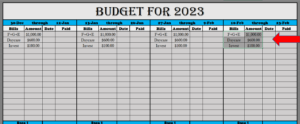

Now to get this to start off accurate you will have to add in whatever money you have left in your account right before you got paid. This will only need to be done for the very first time you do this on the very first budget section, after that this will be automated. So for the example above we added $1,000 in the additional section.

Now to get this to start off accurate you will have to add in whatever money you have left in your account right before you got paid. This will only need to be done for the very first time you do this on the very first budget section, after that this will be automated. So for the example above we added $1,000 in the additional section.

You can see this on the above picture where the first arrow is pointing. Again, this only needs to be done once on the very first section as you are starting your budget. So whatever you have in your bank account right before the Dec 30th pay date, just add that by the “additional” cell.

Paying Your Bills

Once you’ve added your bills in as far out as you want to go, you simply sit down to pay your bills on payday and you’re set for the next 2 weeks until you get paid again.

So what we need to do next is pay bills and then confirm they’ve been paid by using color fills to show they’ve been paid. You also have all of your automated bills highlighted yellow so you know they will automatically come out on their due date.

Use any colors you like, but I personally use green once it has been paid and has come out of my bank account. And if I pay a bill but it hasn’t yet come out of my bank account (pending) I use yellow.

By doing this your budget will be 100% real time matching your actual bank account!

Some bills allow you to pay by a credit/debit card and others only allow a checking account. When you pay with a checking the funds typically won’t come out of your account for a couple of days so by marking this yellow it represents the funds are “pending” and will come out of your account in a day or two.

Some bills allow you to pay by a credit/debit card and others only allow a checking account. When you pay with a checking the funds typically won’t come out of your account for a couple of days so by marking this yellow it represents the funds are “pending” and will come out of your account in a day or two.

Now, also notice how F+G+E changed to only show what you’ve actually spent so far and the remaining estimated amount you will spend changed to “est.” as shown above by the arrow. Again, this keeps you 100% accurate to your checking account in real time.

Does this make sense? In other words, if your estimated F+G+E is $1,000 every 2 weeks and you check your budget halfway through it would be somewhere around $500 already paid on F+G+E and $500 estimated left (est.).

If you pay everything by a credit card (to earn points) and not a debit that is attached to your checking then you would actually just move the “est”. to the next pay period as you would then pay off your credit card balance in full later on.

You Now Have Your Entire 2022 Budget Set Up

You can now scroll down and enter all of your bills for as far out as you want, whether that be a few months or the entire year is up to you.

Notice we haven’t mentioned the “left over” part and that’s because this is automatically calculated. So by placing your bills into the budget template you can now see what you will have left over after every pay period from this pay period to months on out.

So, you’re all set. Your entire budget is now right in front of you for 2022.

Calculating Net Worth

We’ll now move to what I consider the next important section, which is tracking your net worth. What we’re doing here is looking at all of your assets compared to your debts.

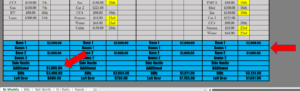

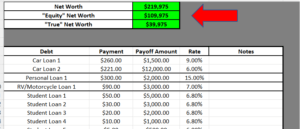

It will give you an output of 3 different measures as scene below:

Now the very top one listed “Net Worth” is the accurate way of tracking your net worth. However, there 2 others included for good reason: “Equity Net Worth” is basically using the equity you have in your primary home as the only dollar number as an asset (not your total home value).

And “True Net Worth” is not considering your primary home value at all as an asset. The reason being for both of these is that typically people have no intentions on downsizing their homes. This just gives you other ways to track your net worth and can give you other goals to set as well. You can read more about why I included these in an article I wrote about net worth here. Keep in mind the top number is the accurate number as to what your net worth is.

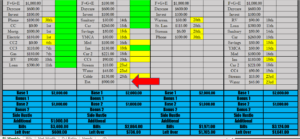

As you can see above you’ll just be adding in all of your debts, the monthly payments, and their total outstanding balance.

In addition to it adding up all of your total debts and monthly payments, it also gives you your credit utilization. The reason for this is because, outside of paying your bills on time, this is one of the most important aspects of your credit score.

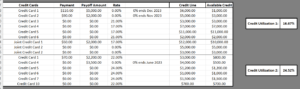

It has an option for yourself and another person as well as “joint” credit cards. In other words, if you and your spouse are both on the same credit card, then this will be on both of your credit reports.

This way you can add in all of your credit cards in your name, your spouse’s credit cards in their name, and any joint cards in both of your names and it will give you the credit utilization separately for each person.

Here is an example of what that will look like:

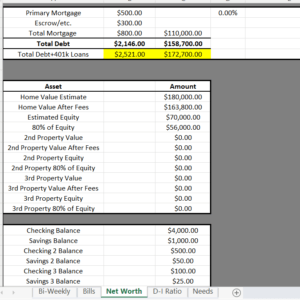

Next, you’ll add in any mortgage or additional outstanding debt you have and it will give you your total debt with the mortgage and without (as well as a total for outstanding obligations that could include 401k loans as these aren’t considered debt).

Then you’ll add in all of your assets.

Your home value after fees, home equity, and 80% of your equity (typical loan max approval) are automatically calculated once you add in your property value. As you can see you can add 2 additional mortgages/properties.

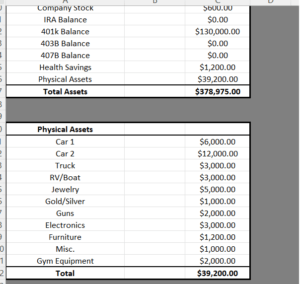

Next you will need to include physical assets as well and it will automatically calculate your total assets.

This gives you a full picture of all your debts compared to your assets. The reason we’re including monthly payments and interest rates on your outstanding debt is because this gives you a full picture of what you need to pay off first or consolidate elsewhere.

Calculating Discretionary Income

To calculate your discretionary income (income left over after paying bills) with this template you’ll need to move back to the “bills” tab. Below where you added in your bills you will now add your bills in by category. It does not include for any savings or investing in this section.

Adding in precheck bills (401k loans, alimony, etc.) will show you the total overall you pay but it won’t be apart of calculating your discretionary income since we’ll be adding our net income below.

With the next section you can add in your net income. It’s important to use net income because at the end of the day, gross income doesn’t really matter. The only thing that matters what you bring home.

An example is shown here:

You simply fill out the section in blue and it will calculate all of the rest.

If you need to calculate your monthly total income off of a weekly or bi-weekly paycheck since there isn’t an even number of weeks/days in every month you can do that here.

As you can see it gives 3 different outputs. This will be dependent on what additional income you have or don’t have coming in.

Again, you may not use these different sections and you can always change the name of each of the but as you can see it will give you an output for your base pay, pay plus any side hustles, and also all of them together which includes any bonuses.

Your template now shows you exactly what your discretionary income is.

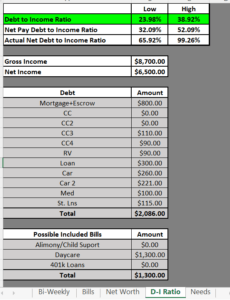

Calculating Your Debt-to-Income Ratio

Calculating your debt-to-income ratio is important not only to know for yourself, but also because lenders will look at this as part of their evaluation as to whether or not they will approve you for a loan.

The template calculates your debt-to-income ratio in the traditional sense, but it also includes a couple more estimates that are more accurate to your real life as they go off of net income:

You’ll just add in your monthly gross income, net income, and monthly bills and it will output your numbers. The top output is your debt-to-income ratio the way it is typically calculated by lenders.

It gives you a low estimate and a high estimate because different lenders include different things. As you can see under “possible included bills” it has some additional debts that may or may not be included depending on what bank you go to. So the answer may lie somewhere in between, and you can fill out the information accordingly to a specific bank’s rules if you want.

Next it will calculate this same number based off of your net income. Again, this is really the number that matters at the end of the day. If you’re looking at this then be sure not to include any bills that already come out of your check since you can already add in net income.

For example, above you see a 401k loan as an option, however if it is automatically taken out of your check and you have it added under “possible included bills” then it will count it twice. Don’t do this.

And finally, it has one more option that really gives you the correct answer as it includes bills that typically are not included as debts:

This is where you’ll get an answer based on all of your bills including utilities, cable, phone, etc. The low % it gives you is simply based off all of your bills and the high percentage is based off of all of your bills and whatever you spend on food, gas, and entertainment as well.

This is the percentage of everything you spend compared to your income. This is just for your records to see where you’re at with your budget. It’s not what any lender will look at.

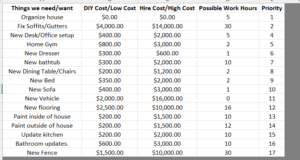

One Additional Tab for What You Plan On Buying in the Future

The last tab is simply to keep track of things you plan on buying. This isn’t generating any type of output formula or anything like that, it’s just giving you a complete insight into your financial budget.

Now you know what you’re planning to buy next and how much your overall expenses will be. Personally, I think this gives you the complete picture of everything you need for a personal budget, which is why I think it’s the best personal budget for myself at least.

How to Edit/Unlock Formulas

All of the formulas are locked to ensure nothing gets messed up or accidentally deleted. If you want to change something you can do that by unprotecting the sheet under the “Review” at the top. You’ll need to use the password: redmoney

And that’s it. That’s everything you need to use this template.

Any thoughts on improvements are welcome. Let me know in the comments below!